There are many savings accounts in South Africa. It can be overwhelming trying to figure out which savings account-type you should be opening first.

For the purposes of this blog post, we will not look at different savings account offers and the competitive interest rates associated with these products. We will instead unpack the four main types of savings accounts/ goals you should consider having.

If you want a closer look at the savings accounts offered and their interest rates at popular banks such as African Bank, Standard Bank, Discovery Bank and Capitec etc, read What is the best savings account for you in South Africa?

The number one savings rule?

When it comes to saving, the number one rule is to save before you spend. What this means is that you should make it a habit to first pay yourself when you get your salary.

It can be tempting to buy the sneakers or go out to eat with friends. However, remember to save first and then indulge.

When selecting savings accounts, consider the following four savings goals:

1. Emergency savings

An emergency savings fund is a savings account with the sole purpose of using the funds when an emergency arises. Here you can think of an emergency like needing to replace the brake pads on your car, losing your job, your geyser bursting or an unexpected tax bill.

This savings account should be:

- Easily accessible (you should have immediate access to your funds)

- Have a low minimum opening deposit

- A total of at least one month’s worth of your salary. Ideally, at least 3 months, but don’t let a big goal delay you from starting. Starting small is better than not starting at all.

Read: Emergency fund: Why and how you should start

2. Short-term savings

The second savings account you should have is a short-term savings account. The purpose of this account should be saving, as the name suggests, for short-term goals.

Have you been eyeing that air-fryer for sometime? Are you saving for your child’s special birthday? This is the savings account you should use as a vehicle to help you achieve your goal.

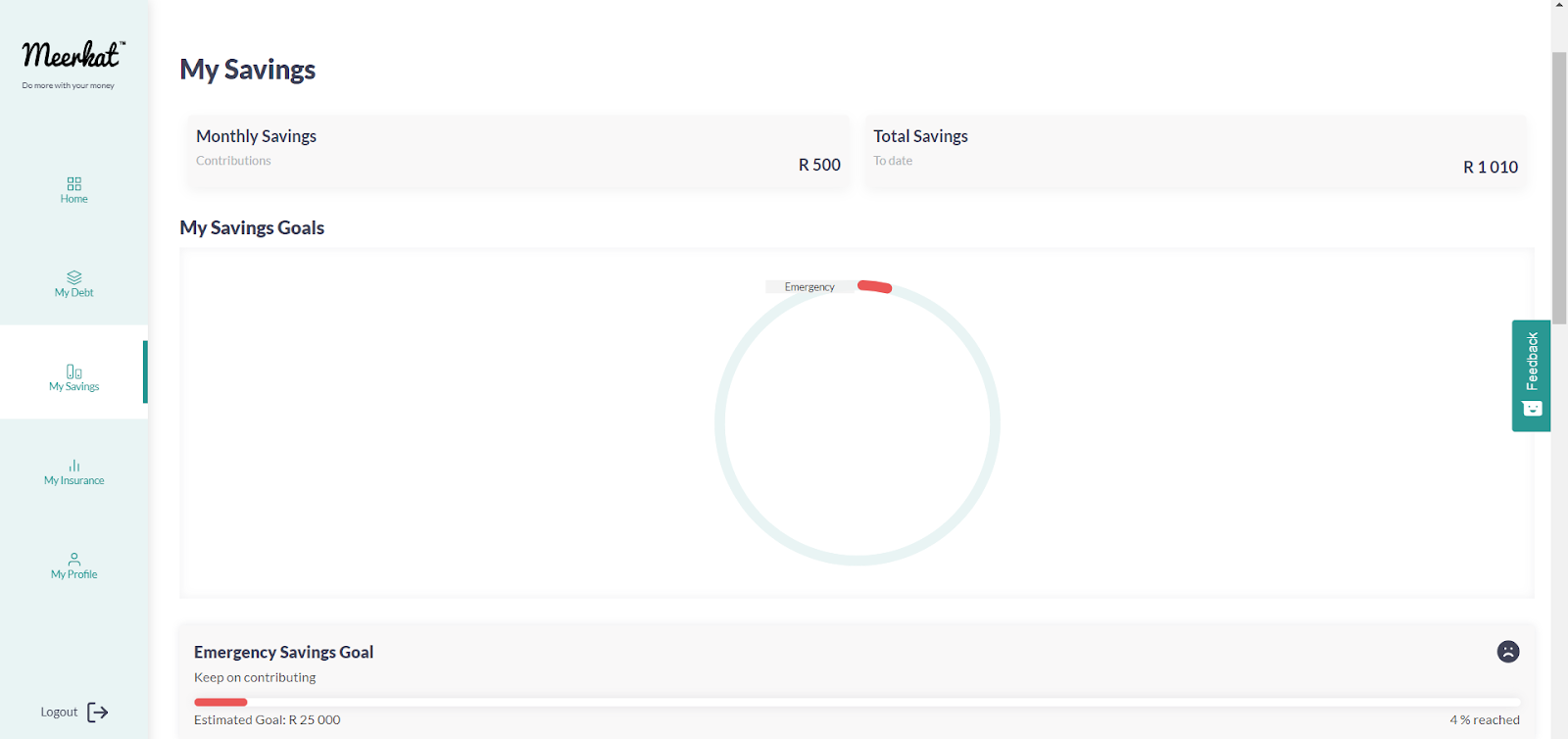

With Meerkat’s online platform you can have access to a complete overview of your financial status. This includes, but is not limited to:

- Each of your savings goals

- Your credit score

- Your affordability level (whether your debt exceeds your affordability level & what you can do about it)

Below is an image of what you could see when you start saving with Meerkat

Using this online platform you can also easily withdraw your funds when you've reached your savings goal or when an emergency arises.

3. Long-term savings

When choosing a savings vehicle, you can also decide to choose one to achieve any long-term savings goals you may have. Examples of these long-term savings goals could be a deposit for a house or car.

With Meerkat, instead of having 3 different accounts you can have ONE savings account for ALL your savings needs.

With Meerkat, you can easily separate your savings goals. This allows you to contribute to each one separately. It also allows you to access the correct funds when you need them.

4. Retirement

Retirement annuities or an RA is a type of investment that allows an individual to save towards retirement.

What’s the difference between a retirement annuity and a pension fund?

A pension fund can only be joined with a company you are employed with. With this fund, you will also be saving towards retirement. Usually, both yourself and your employer will be making regular monthly contributions to the fund. It’s usually offered as a company benefit.

An RA on the other hand, is completely separate from your employer. This is something that you save and contribute towards entirely on your own.

In 2024, the two-pot retirement system will come into effect. The aim of this system is to address pressing short-term financial needs while still preserving money for retirement.

With this system, one third of the money in a retirement fund will be allocated for early access if needed. Whatever money is left in the ‘pot’ will be available as a cash lump sum when the individual retires.

If you find yourself unable to finance your current debt and you’re struggling to make it to the end of the month, instead of using the money you have saved for your retirement, you should consider going under debt review at Meerkat.

“Many employed people consider resigning their jobs to gain access to their pension funds to settle the debts. Unfortunately, this is a temporary short term solution that creates a much bigger long term problem. Many South Africans already have insufficient retirement funds, if you reduce your retirement fund, you are sacrificing capital growth, and will probably never make up the shortfall, no matter how hard you try.

But there is another more sustainable and less painful way. You can consider debt counselling.” - Founder & CEO of Meerkat, David O’Brien

Read: Debt counselling | Everything you need to know